Grocery brands grew revenue in 2025, but profitability took a hit. Price wars replaced promotional tactics as ASP dropped 8.9%. Meanwhile, inventory jumped 41% and Lost Buy Box surged as 3P sellers intensified. The threat shifted from supply chain to marketplace control.

Download the report to see what separated winners from losers in Grocery ecommerce.

Download the full report

Used by the most loved brands in the world

Key takeaways

Inventory funded the growth engine: Brands carried 41.2% more inventory on average, with a sharp H2 build to support online bulk buying and subscription growth

Fulfillment became the competitive advantage: PO Fill Rate sustained 95%+ for most of H2, maintaining operational reliability during peak demand

Price wars replaced promotional tactics: ASP dropped 8.9% as brands lowered base prices to stay competitive, while discount frequency fell 2.7pp, shifting from promotions to permanent price cuts

Traffic growth met strong conversion: Glance views rose 8.2% while conversion improved 10.3pp, driven by repeat subscription customers and consistent product availability

Ad efficiency held while others deteriorated: Return on ad spend (ROAS) remained stable at 3.1x despite ad spend more than doubling in July, making Grocery one of the only categories where paid media maintained efficiency through 2025

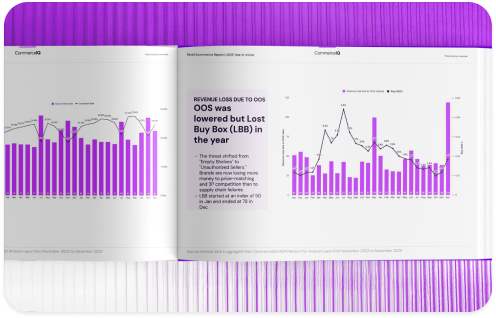

Revenue leakage shifted to unauthorized sellers: Lost Buy Box (LBB) peaked in October as third-party (3P) competition intensified, while reported out of stock (OOS) rate improved 1.8pp, proving the threat moved from supply chain failures to marketplace dynamics