Grocery brands achieved impressive 16% year-over-year sales growth in Q3 2025, outpacing the broader ecommerce average. But beneath the strong revenue numbers, profitability took a significant hit—with unit margins compressing 6.4% as brands absorbed rising costs rather than passing them to price-sensitive shoppers.

Download the full report

Used by the most loved brands in the world

Key takeaways

Strong sales masked eroding profitability: OPS grew 16.8% YoY, but margins fell 6.4% as brands absorbed higher costs and relied on promotional pricing to drive volume.

Inventory build-up paid off for events: A 42% YoY increase in on-hand inventory and 9.3% improvement in fill rates positioned brands to meet demand during tentpole shopping periods.

High-impact stockouts drove major revenue loss: Despite better overall fill rates, revenue lost to OOS surged 108% YoY, indicating critical items were unavailable at peak demand moments.

Ad investments outpaced efficiency gains: Retail media spend jumped 30.2% YoY while ROAS declined 3.8%, showing brands are spending more to hold position rather than gaining ground.

Shoppers showed strong intent despite lower traffic: Glance views dipped just 0.5% YoY, but conversion rates climbed 17%, reflecting more purposeful purchasing behavior.

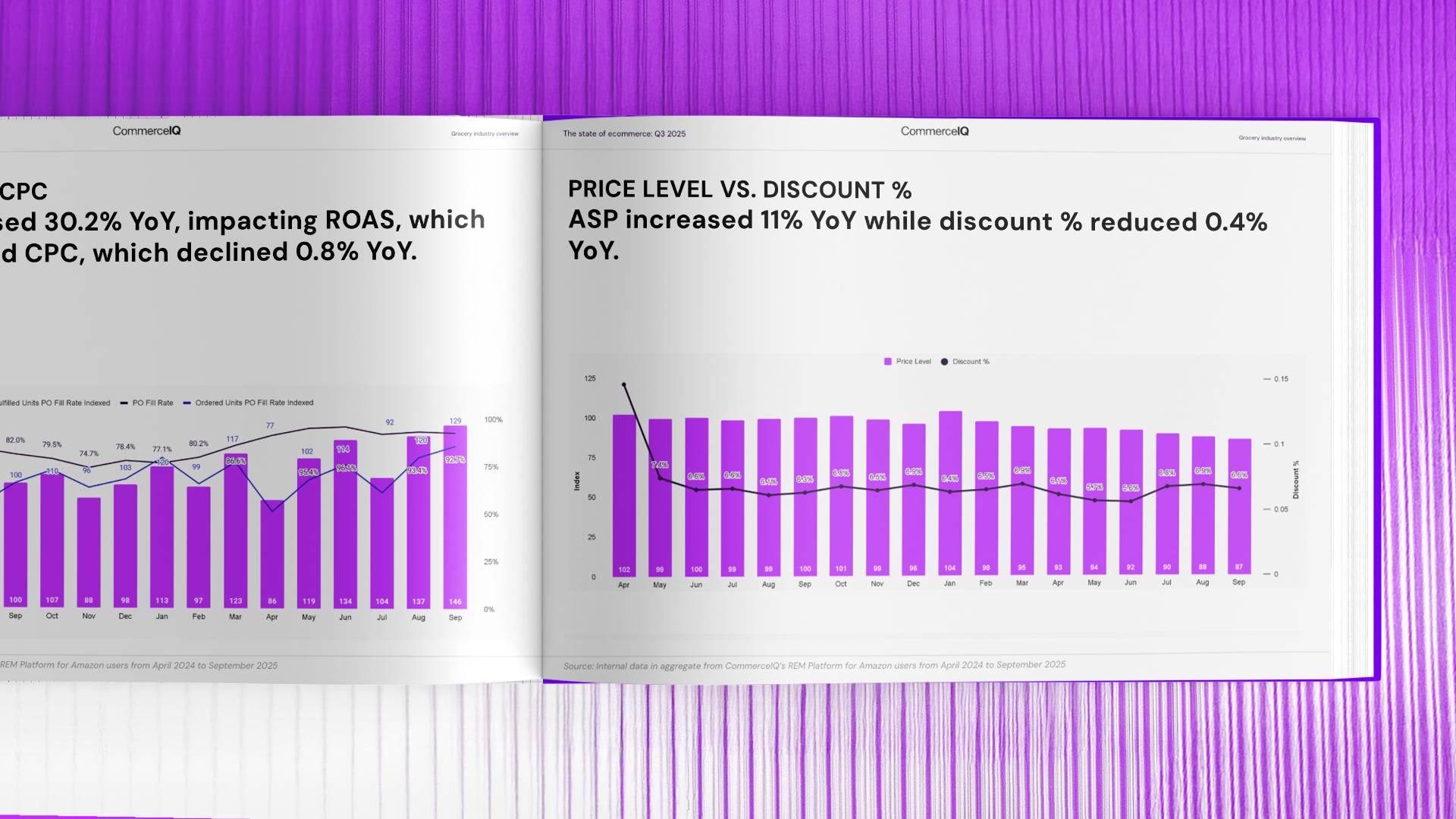

Price increases met with reduced discounting: Average selling price (ASP) rose 11% YoY while discount percentages fell 0.4%, suggesting brands are attempting to preserve margin where possible despite competitive pressure.